Is the Housing Market Going to Crash? Business and Real Estate Outlook for 2026

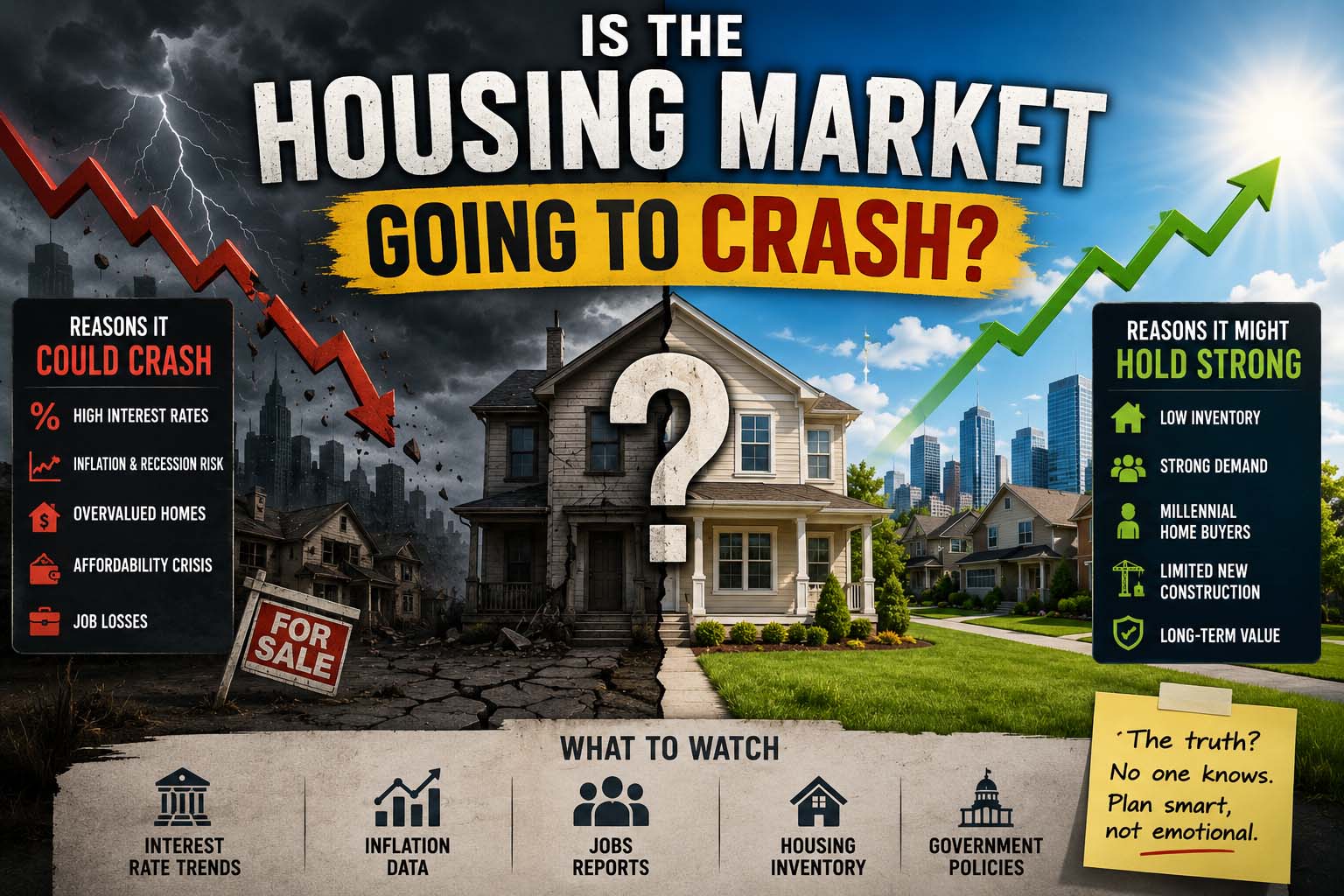

The question “is the housing market going to crash” continues to dominate online searches as buyers, investors, entrepreneurs, and homeowners try to understand the future of real estate. Rising home prices, mortgage interest rates, inflation concerns, and economic uncertainty have created major discussions about whether the market could experience a serious downturn.

In 2026, the housing market remains one of the most important parts of the global economy. Real estate affects banks, businesses, construction companies, investors, and everyday consumers.

While many people fear another major crash similar to 2008, current market conditions are significantly different in several important ways. Understanding those differences can help buyers and business owners make smarter long-term decisions.

Why People Think the Housing Market Could Crash

There are several reasons why concerns about a housing crash continue growing.

Rising Home Prices

Property prices increased rapidly in many countries over the past few years. Some buyers believe homes have become overpriced compared to average incomes.

Higher Mortgage Rates

Mortgage interest rates increased sharply compared to the ultra-low rates seen during previous years. Higher borrowing costs reduce affordability for many buyers.

Inflation and Economic Pressure

Inflation impacts household budgets, making it harder for consumers to save for down payments or qualify for loans.

Slower Buyer Demand

In some markets, buyer activity has cooled because consumers are waiting for better prices or lower interest rates.

These factors create uncertainty, leading many people to ask whether a market correction or crash could happen soon.

Is the Housing Market Going to Crash in 2025?

The keyword “is the housing market going to crash in 2025” gained massive popularity because many analysts predicted a slowdown during that period.

However, most experts observed a cooling market rather than a full collapse.

What Happened in 2025?

In many areas:

Home prices stabilized

Buyer competition decreased

Mortgage demand slowed

Inventory increased slightly

While some cities experienced price reductions, widespread panic selling similar to 2008 did not occur.

This showed that a slower market does not automatically mean a crash.

Is the Housing Market Going to Crash in 2026?

Now, the biggest question has shifted toward “is the housing market going to crash in 2026.”

Most economists believe a nationwide collapse remains unlikely in many major markets. Instead, experts expect regional differences depending on:

Employment growth

Population trends

Interest rates

Housing supply

Local economic conditions

Some cities may see price declines, while others continue growing steadily.

Key Differences Between 2008 and 2026

Many people compare today’s market to the 2008 financial crisis, but there are important differences.

| Factor | 2008 Housing Crisis | 2026 Housing Market |

|---|---|---|

| Lending Standards | Weak | Stricter |

| Mortgage Quality | Risky loans | Higher credit checks |

| Housing Inventory | Oversupply | Limited supply |

| Foreclosures | Extremely high | Lower levels |

| Banking Stability | Fragile | Stronger regulations |

Because lending standards are stricter today, many analysts believe the market is structurally stronger than it was before the last crash.

When Is the Housing Market Going to Crash?

The phrase “when is the housing market going to crash” remains difficult to answer because housing markets rarely collapse overnight.

Most real estate downturns happen gradually.

Signs that analysts watch include:

Sharp unemployment increases

Mass foreclosures

Rapid oversupply

Falling consumer confidence

Major credit problems

Without these conditions, many economists expect slower growth instead of a dramatic crash.

Real-World Examples of Market Slowdowns

Different cities react differently to economic conditions.

Fast-Growing Cities

Cities with strong job markets often maintain housing demand even during slower economic periods.

Overheated Markets

Some locations that experienced rapid price increases may see corrections if affordability becomes too difficult for buyers.

Rural and Smaller Markets

Smaller markets sometimes remain more stable because prices did not rise as aggressively.

These regional differences explain why some areas cool faster than others.

Business Impact of Housing Market Changes

Housing markets influence far more than homebuyers.

Construction Industry

Slower housing demand can reduce construction projects and contractor activity.

Mortgage Businesses

Banks and lenders experience lower loan application volumes during high-interest-rate periods.

Retail and Furniture Companies

Home purchases often increase spending on appliances, furniture, and renovations.

Local Economies

Property taxes and housing development impact city budgets and infrastructure investments.

Because of this, entrepreneurs closely monitor housing trends.

Step-by-Step Guide for Buyers in 2026

Many first-time buyers feel overwhelmed by market uncertainty. The best strategy is focusing on preparation rather than panic.

Step 1: Review Your Budget

Calculate monthly costs carefully before searching for homes.

Step 2: Improve Credit Scores

Better credit helps buyers qualify for stronger mortgage terms.

Step 3: Research Local Markets

National headlines may not reflect conditions in your city.

Step 4: Compare Mortgage Rates

Even small interest rate differences affect long-term affordability.

Step 5: Avoid Emotional Buying

Overpaying because of fear or hype can create financial stress later.

Business Strategy During Housing Uncertaint

Focus on Long-Term Value

Businesses that survive market shifts usually prioritize sustainable growth.

Diversify Investments

Relying entirely on real estate can increase risk.

Watch Interest Rate Trends

Borrowing costs strongly influence housing activity.

Study Local Demand

Some regions remain highly competitive despite national slowdowns.

Smart investors analyze local data rather than reacting only to headlines.

Will Home Prices Drop?

One of the biggest questions connected to housing crash discussions is whether prices will decline significantly.

In many markets, prices may cool or stabilize rather than collapse completely.

Limited housing supply still supports prices in several major cities.

However, areas with weak job growth or excessive speculation could experience stronger corrections.

How Interest Rates Affect the Housing Market

Interest rates play a major role in housing affordability.

Higher mortgage rates increase monthly payments, reducing the number of qualified buyers.

For example:

A small rate increase can add hundreds of dollars to monthly mortgage costs.

This often slows demand and reduces bidding wars.

Housing Supply and Inventory Challenges

One reason experts remain cautious about predicting a crash is limited housing supply.

In many countries, there are still not enough homes available to meet long-term demand.

Low inventory supports prices even during slower economic periods.

This differs from previous housing crashes involving major oversupply.

Should Buyers Wait for a Crash?

Some buyers delay purchases hoping for dramatic price reductions.

However, timing the market perfectly is extremely difficult.

Waiting too long could create risks such as:

Higher interest rates

Rising rents

Missed investment opportunities

For many people, buying based on personal financial readiness matters more than predicting market timing.

FAQ About the Housing Market

Is the housing market going to crash?

Most experts predict slower growth or regional corrections rather than a nationwide collapse.

Some areas may see price declines, but many markets remain supported by low inventory.

There is no confirmed timeline, and crashes usually develop gradually.

The market slowed in some areas during 2025, but a major nationwide crash did not happen.

Should first-time buyers wait?

It depends on financial readiness, local market conditions, and long-term goals.

Conclusion

The question “is the housing market going to crash” will likely remain popular throughout 2026 because economic uncertainty continues influencing buyer confidence and investment decisions.

While some markets may experience corrections or slower growth, current conditions differ significantly from the 2008 housing crisis. Stronger lending standards, limited inventory, and stable employment in many regions provide important support for the market.